The financial assessment of a business is always a topic of debate among financial analysts. Despite accessing identical data, different financial analysts can come up with different company valuations. Non-uniform assumptions and varying levels of optimism cause the results of company value calculations to be different.

Even with a scientific approach to valuing a company, the unpredictability of market reactions remains a significant determinant of its valuation.

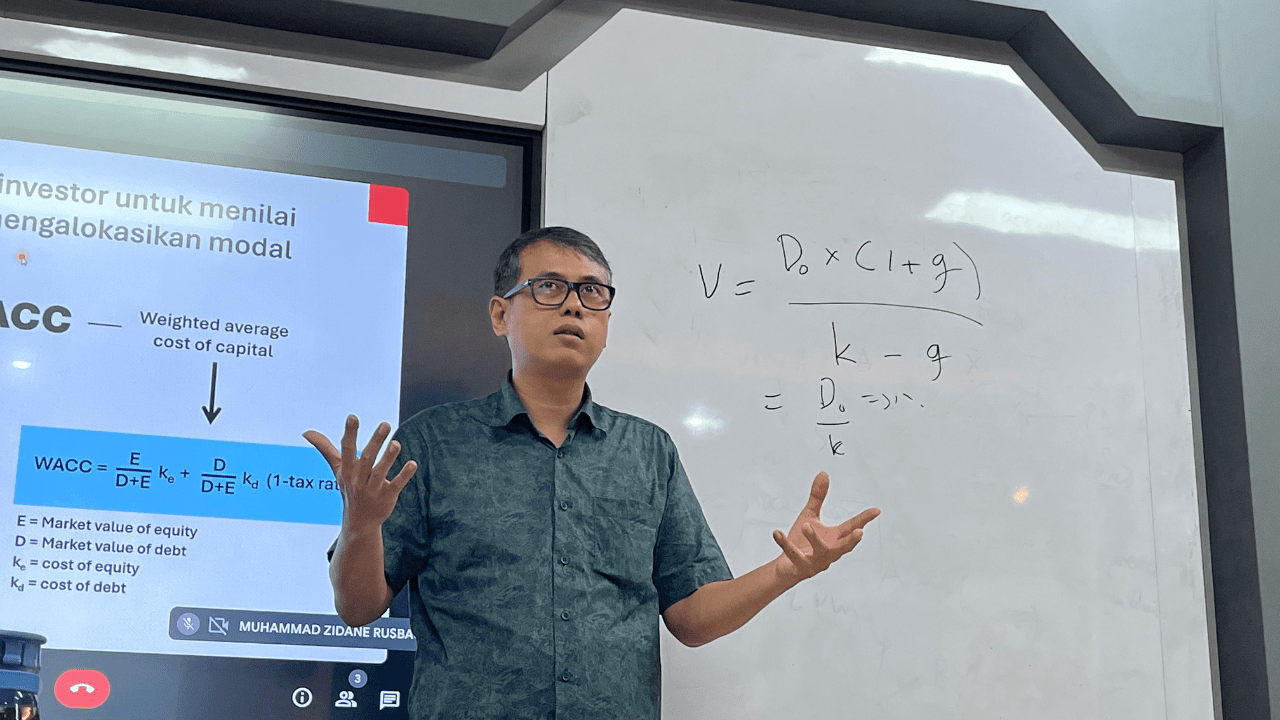

” Theory has its limitations, the real world always presents differences,” said Parahita Irawan, founder of @investasijalanan, during a guest lecture at MBA ITB Bandung on Tuesday (27/2).

On this occasion, Parahita explained the theory and practice of corporate valuation to the students. According to Parahita, Although external factors heavily influence a company’s ultimate value, strategic capital management and business innovation can enhance this value. As a general guideline, companies should always try to keep Return on Invested Capital (ROICC) higher than the Weighted Average Cost of Capital (WACC).

Parahita identified investment, financing, and operational decisions as the three key areas of management decision-making. Appropriate investment and financing choices can lead to higher returns and reduced capital costs.

He referenced Alfred Rappaport, an American economist, to highlight the importance of preserving assets that bolster company value, even at the expense of short-term earnings. This approach elevates the company’s market value and reassures shareholders of the strategic management of capital.

Operational decisions, meanwhile, necessitate innovation within the system. Parahita cited the case of PT Arwana Citramulia Tbk (ARNA), the world’s ninth-largest ceramic producer, as an example. With limited prospects for market growth and sales enhancement, ARNA focused on improving efficiency to boost profits. By innovating in five areas – environment, energy, products, technology, and human resources – ARNA significantly reduced operational costs, achieving a modest 3% sales growth but a substantial 20% increase in net profit between 2019 and 2023.

Parahita concluded the lecture by emphasizing prioritizing long-term value creation over short-term gains.

“While picking low-hanging fruit, don’t forget to construct a ladder to reach the higher fruit,” he concluded, advocating for a balanced approach to growth and value enhancement.